“Simply Put”, the weekly column from the Multi Asset Group team at Lombard Odier Investment Managers

By Florian Ielpo, Head of Macro

Summary:

- The Iran-United States war triggered at the end of February 2026 acts as a global supply shock and a test for American fiscal sustainability

- Academic research confirms that wars temporarily boost GDP and public demand, but generate inflation and a displacement of private capital

- The positive effects are generally localized in defense, energy, small capitalizations but come with a rise in stagflation risk

Florian Ielpo

Florian Ielpo

The war triggered by the United States and Israel against Iran on February 28, 2026, has plunged the global economy into a new phase of uncertainty, far beyond the energy dimension. The Strait of Hormuz, a crucial passage for a fifth of the world’s oil, has become a major strategic tension point. The immediate consequences were a 60% surge in oil prices, a 40-basis-point increase in US interest rates in a few weeks, and a 5 to 8% correction in stock markets. Despite starting this crisis in a moderate position, the US economy faced a real GDP growth of 2% and a PCE inflation of 2.8%. The consensus about a “Goldilocks” economy was put into question. But should we really worry about the effects of this war on the American economy? This is the question raised by Simply Put this week.

A crucial budgetary engine

The literature has long studied the economic effects of armed conflicts, including growth, investment, and rates:

- Growth: Researchers have found that for every dollar of military spending, only 0.6 to 0.9 dollar of GDP is generated due to offsetting effects on employment, production, consumption, and private investment

- Rates: Military spending is usually financed by debt, leading to an increase in public deficits, a steepening of the yield curve, and a rise in inflation

- Investment: Long-term benefits come from increased research and innovation stimulated by public orders, mainly in technology and cybersecurity sectors

In financial economists’ terms, wars represent a “reallocation stimulus”: redistributing wealth rather than creating net value. The conflict with Iran is likely to increase the probability of a moderate stagflation return, characterized by low growth, rising energy costs, and persistent inflation. Let’s review the most visible economic effects of wars led by the United States on its economy.

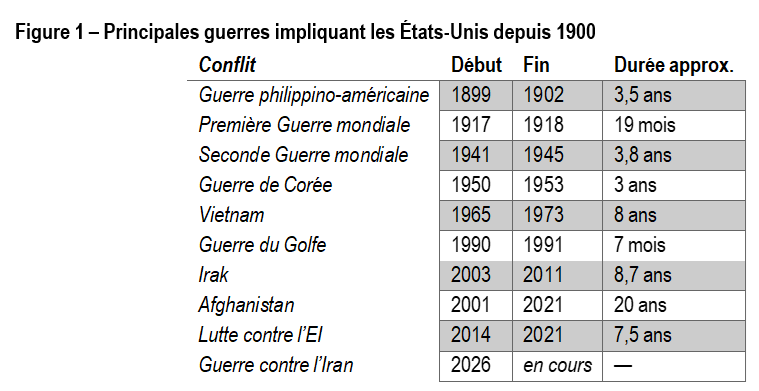

A century of wars and budget constraints

Over the past 120 years, the US has experienced ten major wars, each producing a unique macroeconomic signature: total mobilization (1939-45), overheating (Vietnam), or brief shocks (Gulf 1991). History teaches us that longer and more intense wars lead to durable increases in debt and subsequent inflation. The CBO’s MacFadden R² figure shows that during these phases, the credit rating and sovereign spreads peak after 24 months, indicating that markets can tolerate financial imbalances for a limited time.

The most costly wars do not necessarily result in the most significantly affected markets: the lengthy and less publicized Afghan conflict had a moderate impact on rates, while Vietnam and the Gulf wars caused sharp increases in risk premiums. What actual effects have been observed on the key variables shaping the US economy?

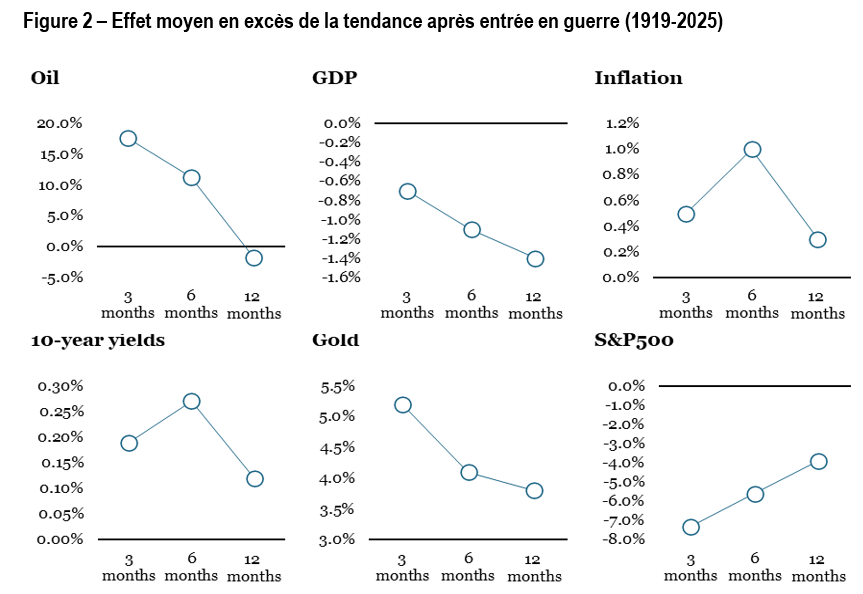

Historical data on US financial markets demonstrate almost mechanical behavior after entering a war. The impact of conflicts on financial markets follows a well-established three-phase sequence: an initial shock period (0-3 months) with high volatility, a significant decline in risky assets, and a surge in commodities; an adjustment phase (3-6 months) with rising sovereign rates, relative stock stabilization but increased credit spreads pressure; finally, a macroeconomic phase (6-12 months) with growth slowdown, inflation peak, revivals in defensive stocks and small capitalizations – all in a context where the stock-bond correlation remains positive, usually reaching its maximum after four years, as observed from 1920 to 2025.

Post-conflict analysis of major financial indicators (1919-2025) confirms the three distinct phases mentioned earlier:

- In the short term (3 months), there is high volatility with a significant decline in stocks (-7.3%), commodity surges (gold +5.2%, oil +17.6%), and rising sovereign rates (+0.19%);

- In the intermediate adjustment phase (6 months), markets stabilize partially with a moderation in stock index decline (-5.6%) but continued pressure on rates (+0.27%);

- Ultimately, over the long term (12 months), macroeconomic effects dominate with a persistent negative GDP deviation from its trend (-1.4 percentage points) and a gradual normalization of credit spreads (-0.04%) – supporting literature observations.

In simple terms, the Iranian war acts as a global energy shock: supporting sector profits but weakening overall growth. In 2026, the United States will be more rearmed than wealthy, more inflationary than prosperous.

Macro/Nowcasting Corner

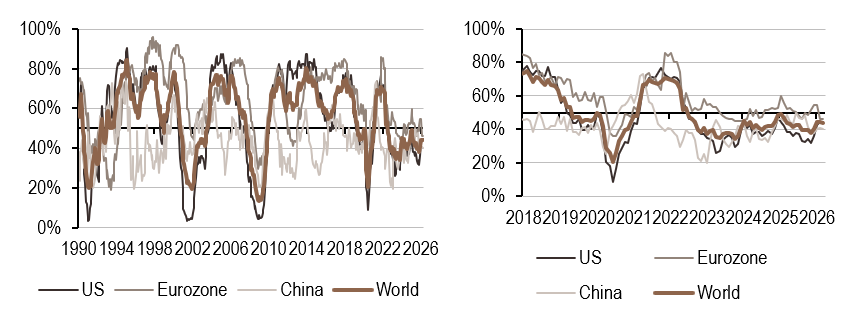

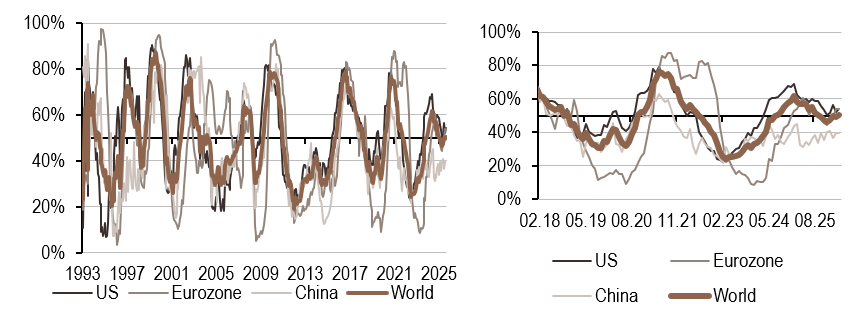

This section presents the latest evolution of our nowcasting indicators for global growth, surprises in global inflation, and surprises in global monetary policy. These indicators track the most recent macroeconomic changes affecting markets.

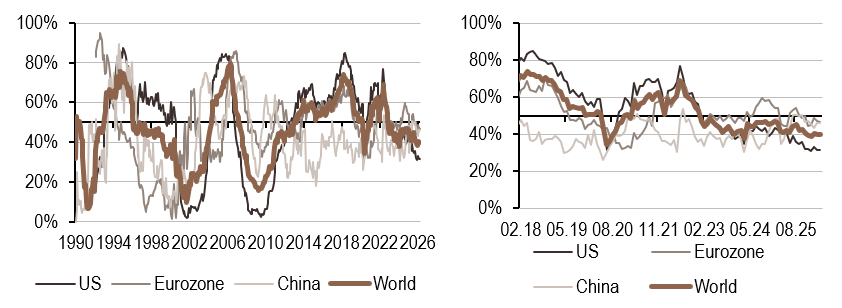

Our nowcasting indicators currently show:

- Global growth nowcaster decreased this week due to the Eurozone, where the regime shifted from high and rising to low and rising. Consumption and employment data deteriorated in this region. China was the only area where the signal slightly improved.

- Our inflation indicator has significantly increased, surpassing the 50% threshold, except in China where it remained unchanged.

- Our global monetary policy signal remained relatively stable. A US increase was offset by a Eurozone signal decrease.

/2026/04/07/69d49e1e21f45286414181.jpg "For the United States, its about connection and trust: How NASA is capitalizing on the Artemis II saga")

{kind=link}